Are consumers really using Buy Now, Pay Later to buy everyday essentials?

Much has been said about Buy Now, Pay Later (BNPL) being used to pay for everyday items like food, groceries and energy bills.

The Observer wrote in January 2022 that consumers were falling into ‘debt traps’ by shopping for everyday essentials with BNPL, noting Zilch, Flava and Clearpay as some of the firms offering repayment plans for supermarketing shopping.

And the Financial Times reported in May 2022 that British households were resorting to BNPL to cover the cost of their rising energy bills, calling out UK-based BNPL firm Zilch for offering repayment plans specifically for household bills.

Perhaps the biggest shake-up from last year came when Deliveroo partnered with Klarna to offer take-away food through Buy Now, Pay Later, a move that was heavily criticised, particularly by Martin Lewis of MoneySavingExpert.

But beyond the headlines, are people really using short-term credit to pay for everyday essentials? And if so, what kind of people are spending this way? Divido asked the public in our latest survey and found some interesting results.

Who is using BNPL to pay for everyday essentials?

In a survey on 1,993 members of the British public conducted in February 2023, Divido found that 8.5% of people have bought food and groceries using finance in the last three years, while 4.5% have used BNPL to pay for household bills.

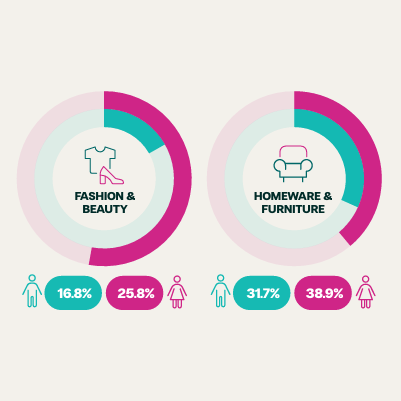

Compared to the 38% who have bought fashion and beauty products, or the 36% who paid for electronics with checkout finance, spending on essentials is therefore comparatively rare.

Who is paying for food and groceries shopping with BNPL?

Drilling into the data, we can analyse the kind of people in the UK who have paid for food and groceries shopping with checkout finance.

First, we note that almost two-thirds (64.7%) of people who have paid for food and groceries with BNPL are female. This is higher than the average of BNPL shoppers, which is 59%.

It is also interesting to note that the majority of food and grocery customers are from younger demographics. 52.9% of shoppers who have bought their shopping through BNPL are in the age group of 18–35 years old. This is higher than the average for this demographic, at 39.1%.

What is noteworthy is that a very high proportion of food and grocery shoppers live in London (31.4%). The overall share of BNPL shoppers in this region is just 12.5%. The second-highest region for food and grocery shoppers is South East England, at 11.8%.

The majority of people who have paid for food and grocery shopping with Buy Now, Pay Later are also from low income households. 55.7% of these shoppers were from households with incomes lower than £25,000. This, again, is higher than the average for this demographic, which is 42.7%.

9.3% of people who have bought shopping through BNPL reported being unemployed, which is almost three times higher than the average for this demographic of 3.3%.

Ultimately, we can conclude that people who shop for food and groceries using checkout finance and Buy Now, Pay Later are more likely to be young, female, living in London, unemployed and from low-income households.

How do food and grocery shoppers perceive BNPL?

At first glance, this seems problematic. However, when we look at the overall sentiment of food and grocery shoppers towards checkout finance, we find that these consumers are generally positive towards finance and budget conscious.

For instance, 88.7% of these consumers agree that they feel comfortable paying with checkout finance, compared to an average of just 55.8%.

86.6% also agree that they use checkout finance as a way to manage their budgets, which is higher than the overall average of 58.3%.

This demographic were also much more likely to use checkout finance for high value transactions (over £1,000), with 82.5% saying they would use checkout finance (far higher than the 50.2% average) compared to 60.9% who said they would use an interest-bearing credit card (lower than the 61.1% average).

Who is paying for household bills using BNPL?

Looking at the demographics who have paid for household bills using checkout finance, we find similar trends.

Once more, females are much more likely to pay for bills using BNPL. 64.7% of those who have paid for their bills using finance are female.

And they tend to be younger too, with 52.9% in the age range 18–35.

London is over-represented once again. 31.4% of people in the UK who have paid for household bills using finance are from London.

So too are lower-income households, with 51.1% of bill-payers coming from households with incomes less than £25,000.

And while a slightly lower proportion claim to be unemployed (7.8%), this is still more than double the average.

What do bill-payers think about using BNPL?

Like food and grocery shoppers, people who have paid for household bills using checkout finance are significantly more likely to agree that BNPL can be used as a good budgeting tool.

When asked if they felt comfortable paying with checkout finance, 82.4% agreed, of which 47.1% strongly agreed. Almost the entire sample (92.9%) also agreed that finance can be used as a way to help them manage their finances – none of this sample disagreed with that statement.

So, once again we find that those who have paid for household bills using checkout finance see it as a budgeting tool and a way to help them make sensible financial decisions.

This demographic were once again more likely to choose BNPL to help them make large transactions. 88.3% said they would use checkout finance to make a transaction over £1,000, compared to 74.5% who would consider using an interest-bearing credit card.

The bottom line

Our survey shows that, despite the headlines, Buy Now, Pay Later is only used by a small percentage of the population to pay for everyday essentials like food and grocery shopping and household bills.

Those who do use finance to manage their everyday expenses are more likely to be young, female, and living in the South East and London. A higher proportion than average are unemployed and from lower-income households.

However, these individuals have a very positive approach to checkout finance and Buy Now, Pay Later. A significant proportion of these spenders view checkout finance as a great way to help them manage their finances, suggesting that they are in control of their spending and simply taking advantage of an often interest-free payment method.

Ultimately, we at Divido would neither encourage people to pay for their food or energy bills with short-term credit, nor facilitate this type of lending. We always say that the lifespan of the loan should not outlast the lifespan of the product. However, we do see the advantage in choosing interest-free credit as a means to manage one’s finances, compared to interest-bearing options such as credit cards and overdrafts.

For now, we are pleased to see that usage of BNPL in the groceries and household bills sector is low and urge anyone thinking of using short-term credit to pay for everyday essentials to only do so if they are well-informed about the potential risks.

Get the full picture today

This is just a taste of the incredible insights we’ve uncovered in our latest survey. If you want to discover not just where customers are shopping with checkout finance, but how much they are spending, and how they feel about this new form of payment, download your free copy of the report today.

Keen to know more?