Merchants must adapt to BNPL and the changing nature of retail finance

Merchants are not just seeking more customers, but also the right customers. Those who had previously dismissed BNPL as appealing only to Gen Z or those unable to get credit elsewhere are now seeing demand across demographic segments for flexible ways to pay.

Estimates put the size of the global BNPL market at $3.98 trillion by 2030, a growth of 45% per year. In the US alone, adoption is on the up: in a recent survey 20% of consumers said they had used BNPL in 2021, with 52% interested in doing so in 2022.

The temptation is to see BNPL as a young person’s payment preference, or for those on low incomes who struggle to access more traditional credit. This is because it seems designed for those seeking instant shopping gratification, or wanting to (or needing to) avoid the costs, checks and hassle associated with more traditional lines of credit. BNPL is commonly associated with short repayment terms (typically 30 days to 3 months); is used for relatively inexpensive purchases (usually £200 and under); with no interest payable on the loan; and currently subjected to less regulatory scrutiny, so no legally mandated consumer protection measures, such as creditworthiness or affordability checks.

On the one hand, this is true. BNPL is popular with these cohorts: almost a third of Gen Z (those 25 years old and under) use it, and slightly more (34%) for those who struggle to pay their bills. In APAC, BNPL optionality at the checkout has become a key reason in itself to shop online for the under 30s.

Presumption is risky

But this does not exclude others, and merchants who presume that their customers have no appetite for BNPL could be in for a rude awakening. People of all ages and affluence are jumping at the chance to use BNPL as another opportunity (alongside credit cards and traditional retail finance products) to spread the cost of their purchases, manage their cash flow smarter and take advantage of zero percent financing. The latter is becoming more relevant to customers as interest rates trend up.

Research into the US market suggests there is very little difference in BNPL usage amongst 18-44 year olds, and only a slight drop off after that. While another study suggests Millennials (aged 26-41) are actually more inclined than Gen Z to shop with BNPL (34% vs 30%).

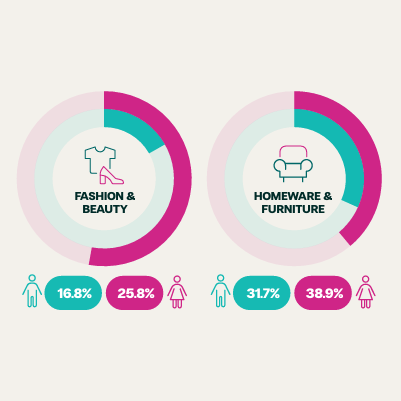

Neither is income a determinant of BNPL use; in fact, the more you earn, the more you are likely to choose it—almost a quarter for people earning more than $100k a year versus 15% for those earning less than $50k. Social class should be discounted too; 63% of BNPL users are in full-time employment, and 40% have a university degree or higher. Creditworthiness (or the lack of it) is also a red herring for BNPL use; 68% of people who use BNPL also have access to a credit card.

Insights that go to the bottom line

So merchants that ignore BNPL on the grounds that they have a more mature and affluent customer base risk losing sales as a result.

What’s more, it seems a taste of BNPL leaves you wanting more: 92% of the consumers who use BNPL more than once a week say they are highly interested in using it again, as did 65% of once-a-month users and 43% of once-a-year users.

The data is clear. Merchants cannot afford to ignore BNPL. Those that do will find it harder to attract, convert and retain customers who increasingly expect to pay in their preferred way. Conversely, merchants that get behind BNPL have much to gain. Klarna, a major BNPL provider, found an increase of 58% in average order value and 30% in conversion rates for merchants using its service.

More, but balanced

At the same time, merchants cannot abandon customers who want to stick with the credit methods they know. This includes retail finance with longer repayment periods (typically at least one year) and predictable interest rates (and sometimes 12 months interest free), and which are subject to security of ID, affordability and credit checks. Our own insights estimate that, in the UK alone, the biggest five traditional retail finance companies loan out almost £5bn in credit every year.

The takeaway for merchants is not to presume what type of credit people prefer, but instead provide a broad suite of options so that a customer can be matched with the most appropriate lending solution for them. In doing so a merchant should consider a number of factors; the profile of their customer, the price point of the product, the cost of the lender’s fee and the final profit margin being the most obvious ones. That will deliver different conclusions as to which lending product will benefit the customer and merchant alike. Sometimes it will be a monthly instalment product, with a range of payment periods – 6, 12, 24 months – and with clear monthly costs. Top up loans may also be attractive and appropriate. Merchants should also think beyond the initial sale, to consider how easy it is for a loan supplier to raise a customer’s credit limit, allowing them to buy associated extras, such as a service plan or accessory set.

That said, there is a balance. Switching on new credit offers, be it BNPL or instalment plans, is not without effort or risk. Merchants will need to work out the optimum number of lenders and products to offer to avoid decision fatigue. They should also consider which providers they use to offer these, to ensure they are maximising sales whilst maintaining assurance over their customers’ data and their brand. (These considerations were covered in a previous article by Divido.)

Get the balance right, and the benefit goes well beyond the immediate conversion. Customers with the right lending product behind them have the means, and the will, to spend more.

The trust factor

For some shoppers, any BNPL product will suffice; for others, convenience needs to be matched by trust in the merchant. Indeed, trust is considered by most people (53%) to be an important factor when deciding to use a short-term credit payment method. In other words, merchants who fail to communicate trust at the checkout should not expect BNPL to be the golden goose. Merchants should also consider the post-checkout experience, especially how to nurture ongoing customer engagement and loyalty once a third party BNPL provider has entered the scene.

How merchants can foster trust and engagement at all stages of the customer and payment journey, and use BNPL as a competitive advantage, will be the subject of the next articles in this series.

Divido’s whitelabel retail finance platform helps merchant’s take back control of their brand experience and customer journey. Our award winning technology is powering the retail finance programs for some of the world’s leading retailers.

Keen to know more?